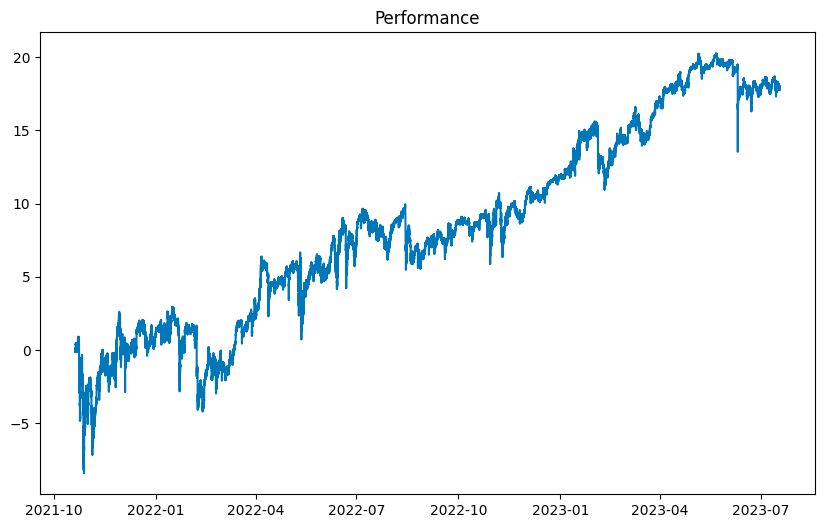

Realistic Backtester for Perpetual Futures (Part 1/2) (With Code)

A guide to writing a realistic market simulator for Crypto perpetual futures.

Table of Contents

Part 1:

Introduction

Simulator/backtester architecture

Preparing the data

Simulating a single market

Simulating market orders

Part 2:

Simulating trading costs

Simulating funding

Simulating many markets

Finish

Subscriber materials (source code)

Introduction

In the last article, we looked at how markets work and at simulating them in theory.

Today we w…